graph TD

A[Multiple Regression<br/>and Correlation] --> B[The Multiple<br/>Regression Model]

A --> C[Multicollinearity]

A --> D[Dummy Variables]

A --> E[Curvilinear Models]

B --> B1[Standard Error<br/>of Estimation]

B --> B2[Coefficient of<br/>Determination]

B --> B3[Adjusted Coefficient<br/>of Determination]

C --> C1[Problems]

C --> C2[Detection]

C --> C3[Treatments]

E --> E1[Polynomial<br/>Models]

E --> E2[Logarithmic<br/>Models]

style A fill:#e1f5ff

style B fill:#fff4e1

style C fill:#ffe1e1

style D fill:#e1ffe1

style E fill:#f0e1ff

13 Chapter 12: Multiple Regression and Correlation

13.1 Opening Scenario: Griffen Associates’ Competitive Analysis

As you prepare for your graduation later this year, you’ve taken on an internship position with Griffen Associates, a prominent investment firm in Chicago. As a measure of your financial acumen, the company has entrusted you with the task of analyzing the market performance of mutual funds that compete with Griffen’s offerings. Data has been collected for the three-year return (R3A) and one-year return (R1A) for 15 competing funds.

Mr. Griffen has requested a comprehensive report on the performance of these competitors, based on various factors including their rates of return, total assets, and whether each fund carries a sales load charge.

There is particular interest at Griffen Associates in determining whether there has been any significant change over the past three years in the performance of these funds. Griffen is considering major changes to many of its operational procedures, and several managers who have been with the firm for years are concerned about the outcomes of such changes. By analyzing the behavior of competing firms over time, these managers hope to gain insights into the future direction of Griffen Associates.

This project will require you to configure and analyze a multiple regression model that can provide the necessary information to inform the critical operational procedures that Griffen Associates is considering implementing.

13.2 Learning Objectives

After completing this chapter, you will be able to:

- Understand multiple regression models and how they extend simple linear regression to include two or more independent variables

- Interpret partial regression coefficients and their meaning in the context of holding other variables constant

- Calculate and interpret the standard error of estimation for multiple regression models

- Evaluate model quality using the coefficient of multiple determination (R^2) and adjusted R^2

- Conduct ANOVA tests to assess overall model significance

- Perform hypothesis tests for individual regression coefficients

- Detect and address multicollinearity problems in multiple regression

- Apply dummy variables to incorporate qualitative factors into regression models

- Understand curvilinear models including polynomial and logarithmic transformations

- Make informed business decisions using multiple regression analysis results

13.3 Chapter Structure

13.4 12.1 Introduction to Multiple Regression

In Chapter 11, we examined how a single explanatory variable could be used to predict the value of a dependent variable. Consider how much more powerful the model could become if we used more explanatory variables. This is precisely what the multiple regression model accomplishes—it allows us to incorporate two or more independent variables into our analysis.

13.4.1 Why Multiple Regression?

In the real world of business, outcomes are rarely determined by a single factor. Consider these examples:

- Sales revenue might depend on advertising expenditure, number of salespeople, price levels, and economic conditions

- Housing prices are influenced by square footage, number of bedrooms, location, age of the home, and neighborhood quality

- Student performance may be affected by study hours, class attendance, previous academic achievement, and socioeconomic factors

- Employee productivity could be related to training hours, experience, compensation, and work environment

Simple regression, while useful, provides an incomplete picture when multiple factors influence the dependent variable. Multiple regression allows us to:

- Increase explanatory power: By including relevant variables, we can explain more of the variation in Y

- Control for confounding factors: We can isolate the effect of one variable while holding others constant

- Make better predictions: More information typically leads to more accurate forecasts

- Test complex hypotheses: We can examine how multiple factors work together

13.4.2 The General Multiple Regression Model

NoteThe Multiple Regression Model

The population multiple regression model with k independent variables is expressed as:

Y = \beta_0 + \beta_1X_1 + \beta_2X_2 + \cdots + \beta_kX_k + \varepsilon

Where:

- Y = Dependent variable (the outcome we want to predict) - X_1, X_2, \ldots, X_k = Independent variables (predictors or explanatory variables) - \beta_0 = Population intercept (value of Y when all X_i = 0) - \beta_1, \beta_2, \ldots, \beta_k = Population regression coefficients - \varepsilon = Random error term (captures unexplained variation) - k = Number of independent variables

Using sample data, we estimate this model as:

ImportantThe Estimated Multiple Regression Model

\hat{Y} = b_0 + b_1X_1 + b_2X_2 + \cdots + b_kX_k

Where:

- \hat{Y} = Predicted value of the dependent variable - b_0 = Sample estimate of the intercept - b_1, b_2, \ldots, b_k = Sample estimates of the regression coefficients (called partial or net regression coefficients)

13.4.3 Understanding Partial Regression Coefficients

The key concept in multiple regression is the interpretation of the partial regression coefficients. Each coefficient b_i represents:

The change in Y associated with a one-unit change in X_i, holding all other independent variables constant.

This “holding constant” or “ceteris paribus” condition is what distinguishes multiple regression from simple regression. Let’s illustrate with an example.

Example 12.1: Interpreting Partial Coefficients

Suppose a real estate model produces:

\text{Price} = 50,000 + 75 \times \text{SquareFeet} + 15,000 \times \text{Bedrooms}

Interpretation:

- Intercept (b_0 = 50,000): The base price when both square feet and bedrooms equal zero (often not meaningful in practical terms, but mathematically necessary)

- Square Feet Coefficient (b_1 = 75): For each additional square foot, the house price increases by $75, assuming the number of bedrooms remains unchanged

- Bedrooms Coefficient (b_2 = 15,000): For each additional bedroom, the house price increases by $15,000, assuming the square footage remains unchanged

This interpretation is crucial. The coefficient for square feet ($75) is not the same as it would be in a simple regression with only square feet—it has been adjusted to account for the presence of bedrooms in the model.

13.5 12.2 Assumptions of Multiple Regression

Multiple regression inherits all the assumptions from simple linear regression, plus two additional requirements critical for valid inference.

13.5.1 Standard Assumptions (from Simple Regression)

- Linearity: The relationship between Y and each X_i is linear

- Independence: Observations are independent of each other

- Homoscedasticity: The variance of errors is constant across all levels of the independent variables

- Normality: The errors (\varepsilon) are normally distributed with mean zero

13.5.2 Additional Assumptions for Multiple Regression

Assumption 5: Sufficient Sample Size

WarningSample Size Requirement

The number of observations n must exceed the number of independent variables k by at least 2:

n \geq k + 2

Why? In multiple regression, we estimate k + 1 parameters (the k coefficients plus the intercept b_0). The degrees of freedom are:

\text{df} = n - (k + 1) = n - k - 1

To retain at least one degree of freedom: n - k - 1 \geq 1, which means n \geq k + 2.

Practical Guidelines: - Minimum: n \geq k + 2 (absolute minimum) - Adequate: n \geq 5(k + 1) (at least 5 observations per parameter) - Preferred: n \geq 10(k + 1) (at least 10 observations per parameter) - Ideal: n \geq 20(k + 1) (at least 20 observations per parameter)

Assumption 6: No Perfect Multicollinearity

ImportantMulticollinearity

Multicollinearity exists when two or more independent variables are linearly related to each other.

Perfect multicollinearity examples: - X_1 = X_2 + X_3 (one variable is an exact linear combination of others) - X_1 = 0.5X_2 (one variable is a constant multiple of another) - X_3 = 100 for all observations (a variable has no variation)

Why is this a problem?

When independent variables are highly correlated with each other, the regression cannot uniquely determine each variable’s individual contribution to explaining Y. This can cause:

- Sign reversals: Coefficients may have the opposite sign from what logic dictates

- Large standard errors: Coefficients become statistically insignificant even when the model as a whole is significant

- Unstable estimates: Small changes in data can produce large changes in coefficients

- Difficulty interpreting results: The “holding other variables constant” interpretation breaks down

Example 12.2: Multicollinearity Problem

Imagine trying to predict salary (Y) using: - X_1 = Years of experience - X_2 = Age

These variables are highly correlated (older workers generally have more experience). If we include both: - The model might show a negative coefficient for experience (illogical!) - Standard errors will be inflated - Neither variable might appear significant, even though together they are

Solution: Include only one of the correlated variables, or combine them in some meaningful way.

We will explore multicollinearity detection and remedies in detail later in this chapter (Section 12.6).

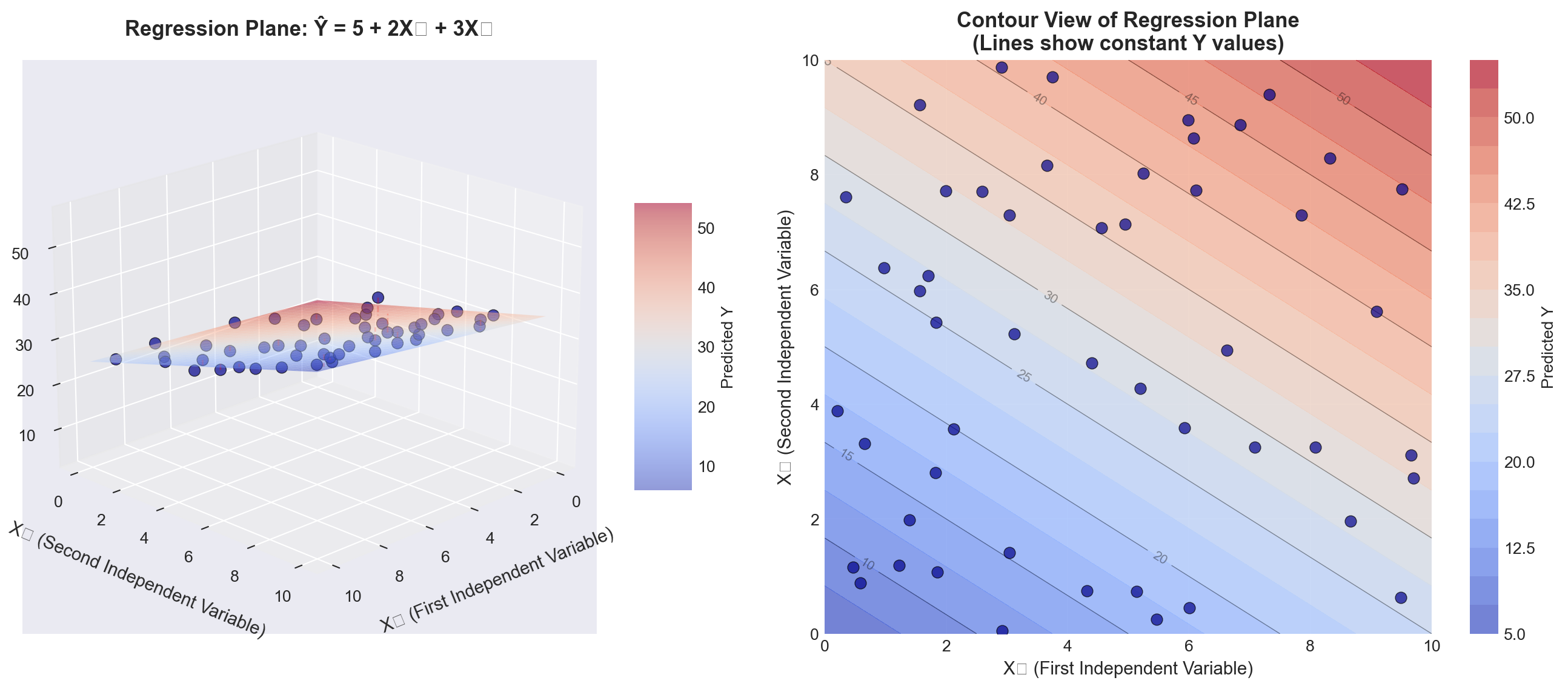

13.6 12.3 The Regression Plane and Hyperplane

13.6.1 Two Independent Variables: The Regression Plane

When we have exactly two independent variables, we can visualize the regression model as a plane in three-dimensional space:

\hat{Y} = b_0 + b_1X_1 + b_2X_2

Code

import numpy as np

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

np.random.seed(42)

# Create figure with 3D subplot

fig = plt.figure(figsize=(14, 6))

# First subplot: Regression plane with scattered points

ax1 = fig.add_subplot(121, projection='3d')

# Generate sample data for the plane

n_points = 50

X1 = np.random.uniform(0, 10, n_points)

X2 = np.random.uniform(0, 10, n_points)

# True model: Y = 5 + 2*X1 + 3*X2 + error

Y = 5 + 2*X1 + 3*X2 + np.random.normal(0, 2, n_points)

# Create mesh for the regression plane

X1_mesh = np.linspace(0, 10, 30)

X2_mesh = np.linspace(0, 10, 30)

X1_grid, X2_grid = np.meshgrid(X1_mesh, X2_mesh)

Y_grid = 5 + 2*X1_grid + 3*X2_grid

# Plot the regression plane

surf = ax1.plot_surface(X1_grid, X2_grid, Y_grid, alpha=0.5,

cmap=cm.coolwarm, edgecolor='none')

# Plot the scattered data points

scatter = ax1.scatter(X1, X2, Y, c='darkblue', marker='o', s=50,

alpha=0.7, edgecolors='black', linewidth=0.5)

# Draw vertical lines from points to plane (residuals)

for i in range(0, n_points, 3): # Show every 3rd residual to avoid clutter

Y_pred_i = 5 + 2*X1[i] + 3*X2[i]

ax1.plot([X1[i], X1[i]], [X2[i], X2[i]], [Y[i], Y_pred_i],

'r--', alpha=0.3, linewidth=1)

ax1.set_xlabel('X₁ (First Independent Variable)', fontsize=11, labelpad=10)

ax1.set_ylabel('X₂ (Second Independent Variable)', fontsize=11, labelpad=10)

ax1.set_zlabel('Y (Dependent Variable)', fontsize=11, labelpad=10)

ax1.set_title('Regression Plane: Ŷ = 5 + 2X₁ + 3X₂', fontsize=13, fontweight='bold', pad=15)

ax1.view_init(elev=20, azim=45)

# Add colorbar

cbar = fig.colorbar(surf, ax=ax1, shrink=0.5, aspect=5)

cbar.set_label('Predicted Y', fontsize=10)

# Second subplot: Contour view (bird's eye view)

ax2 = fig.add_subplot(122)

# Create contour plot

contour = ax2.contourf(X1_grid, X2_grid, Y_grid, levels=20, cmap=cm.coolwarm, alpha=0.7)

contour_lines = ax2.contour(X1_grid, X2_grid, Y_grid, levels=10, colors='black',

linewidths=0.5, alpha=0.4)

ax2.clabel(contour_lines, inline=True, fontsize=8, fmt='%.0f')

# Plot data points on contour

ax2.scatter(X1, X2, c='darkblue', marker='o', s=50, alpha=0.7,

edgecolors='black', linewidth=0.5, zorder=5)

ax2.set_xlabel('X₁ (First Independent Variable)', fontsize=11)

ax2.set_ylabel('X₂ (Second Independent Variable)', fontsize=11)

ax2.set_title('Contour View of Regression Plane\n(Lines show constant Y values)',

fontsize=13, fontweight='bold')

ax2.grid(True, alpha=0.3)

# Add colorbar for contour plot

cbar2 = fig.colorbar(contour, ax=ax2)

cbar2.set_label('Predicted Y', fontsize=10)

plt.tight_layout()

plt.show()

TipInterpreting the Regression Plane

Left panel (3D view): - The blue surface is the regression plane defined by \hat{Y} = b_0 + b_1X_1 + b_2X_2 - The dark blue points are actual observations - The red dashed lines represent residuals (vertical distances from points to the plane) - The plane slopes upward as both X_1 and X_2 increase (positive coefficients)

Right panel (Contour view): - Each curved line represents points on the plane with the same Y value - The spacing between contour lines shows the rate of change - This “bird’s eye view” helps visualize the joint relationship of X_1 and X_2 with Y

Key insight: The regression plane minimizes the sum of squared vertical distances (residuals) from all points to the plane, just as the regression line did in simple regression.

13.6.2 Three or More Variables: The Hyperplane

When we have three or more independent variables (k \geq 3), the model becomes:

\hat{Y} = b_0 + b_1X_1 + b_2X_2 + b_3X_3 + \cdots + b_kX_k

This represents a hyperplane in (k+1)-dimensional space: - One dimension for Y - k dimensions for the independent variables X_1, X_2, \ldots, X_k

Visualization challenge: We cannot directly visualize 4-dimensional space or higher. However: - The mathematical principles remain identical - We can visualize slices of the hyperplane (holding some variables constant) - We can examine pairwise relationships through multiple 2D plots - Statistical software handles the high-dimensional calculations

13.7 12.4 From Simple to Multiple: What Changes?

Let’s compare simple and multiple regression to understand the transition:

| Aspect | Simple Regression | Multiple Regression |

|---|---|---|

| Model form | \hat{Y} = b_0 + b_1X | \hat{Y} = b_0 + b_1X_1 + b_2X_2 + \cdots + b_kX_k |

| Geometric representation | Line in 2D space | Plane (k=2) or hyperplane (k≥3) |

| Coefficient interpretation | Change in Y per unit change in X | Change in Y per unit change in X_i, holding all other X_j constant |

| Degrees of freedom | n - 2 | n - k - 1 |

| Number of parameters | 2 (b_0, b_1) | k + 1 (b_0, b_1, \ldots, b_k) |

| Determination coefficient | r^2 | R^2 |

| Potential problems | Omitted variable bias | Multicollinearity, overfitting |

| Manual calculation | Feasible | Very tedious; computer required |

13.8 Section Exercises

12.1 Given the multiple regression model \hat{Y} = 40 + 3X_1 - 4X_2: a. Interpret each coefficient in the model

b. Estimate Y when X_1 = 5 and X_2 = 10

c. What happens to \hat{Y} if X_1 increases by 2 units while X_2 remains constant?

12.2 A marketing analyst develops a model to predict monthly sales (in thousands):

\text{Sales} = 50 + 1.2 \times \text{Advertising} + 0.8 \times \text{Salespeople} - 2.5 \times \text{Price}

- Interpret the coefficient for Advertising

- Interpret the coefficient for Price (why is it negative?)

- Predict sales when Advertising = $10,000, Salespeople = 5, and Price = $20

12.3 Explain in your own words what “holding other variables constant” means in the context of multiple regression coefficients.

12.4 A student runs a regression with 50 observations and 6 independent variables.

a. How many degrees of freedom does this model have?

b. Is the sample size adequate? Explain using the guidelines provided.

12.5 Consider the following regression equation with t-values in parentheses: \hat{Y} = 100 + 17X_1 + 80X_2 (0.73) \quad (6.21)

- Which variable appears to be statistically significant?

- How might you improve this model?

12.6 For the equation \hat{Y} = 100 - 20X_1 - 40X_2:

a. What is the estimated impact of X_1 on Y?

b. What conditions regarding X_2 must be observed when answering part (a)?

12.7 A demand function is expressed as: \hat{Q} = 10 + 12P + 8I where Q is quantity demanded, P is price, and I is consumer income.

a. Does the sign on the price coefficient make economic sense? Explain

b. What does this suggest about potential problems with this model?

12.8 Explain the difference between:

a. The population regression model and the estimated regression model

b. Simple regression coefficients and partial regression coefficients

c. Perfect multicollinearity and high multicollinearity

12.9 True or False (explain your reasoning):

a. Adding more independent variables always improves a regression model

b. In multiple regression, each coefficient measures the total effect of that variable on Y

c. You can always visualize multiple regression models in three dimensions

d. Multiple regression requires more observations than simple regression

12.10 A researcher wants to predict house prices using: - Square footage - Number of bedrooms

- Age of house - Distance from city center - School district quality (rated 1-10) - Crime rate in neighborhood

- Write out the general form of this multiple regression model

- How many parameters need to be estimated?

- What would be a reasonable minimum sample size for this study?

- Give an example of two variables that might be highly correlated (multicollinearity concern)

Key Terms Introduced: - Multiple regression model - Partial (net) regression coefficients - Regression plane - Hyperplane - Multicollinearity - Degrees of freedom in multiple regression

In Chapter 11, Hop Scotch Airlines used advertising in a simple regression model to explain and predict the number of passengers. That model achieved an impressive standard error of 0.907 and an r^2 of 94%. However, management believes they can improve the model’s explanatory power by incorporating additional relevant variables.

13.8.1 Expanding the Model

Recognizing that income is a primary determinant of demand for air travel, Hop Scotch decides to include national income as a second explanatory variable. The reasoning is sound from both a theoretical and business perspective:

- Higher national income → More disposable income for consumers

- More disposable income → Greater ability to purchase air travel

- Income and advertising may work together → Combined effect on passengers

The multiple regression model for Hop Scotch becomes:

NoteHop Scotch Airlines Multiple Regression Model

\hat{Y} = b_0 + b_1X_1 + b_2X_2

Where:

- \hat{Y} = Projected number of passengers (in thousands) - X_1 = Advertising expenditure (in hundreds of dollars) - X_2 = National income (in trillions of dollars) - b_0 = Intercept (baseline passengers when both variables equal zero) - b_1 = Partial regression coefficient for advertising - b_2 = Partial regression coefficient for national income

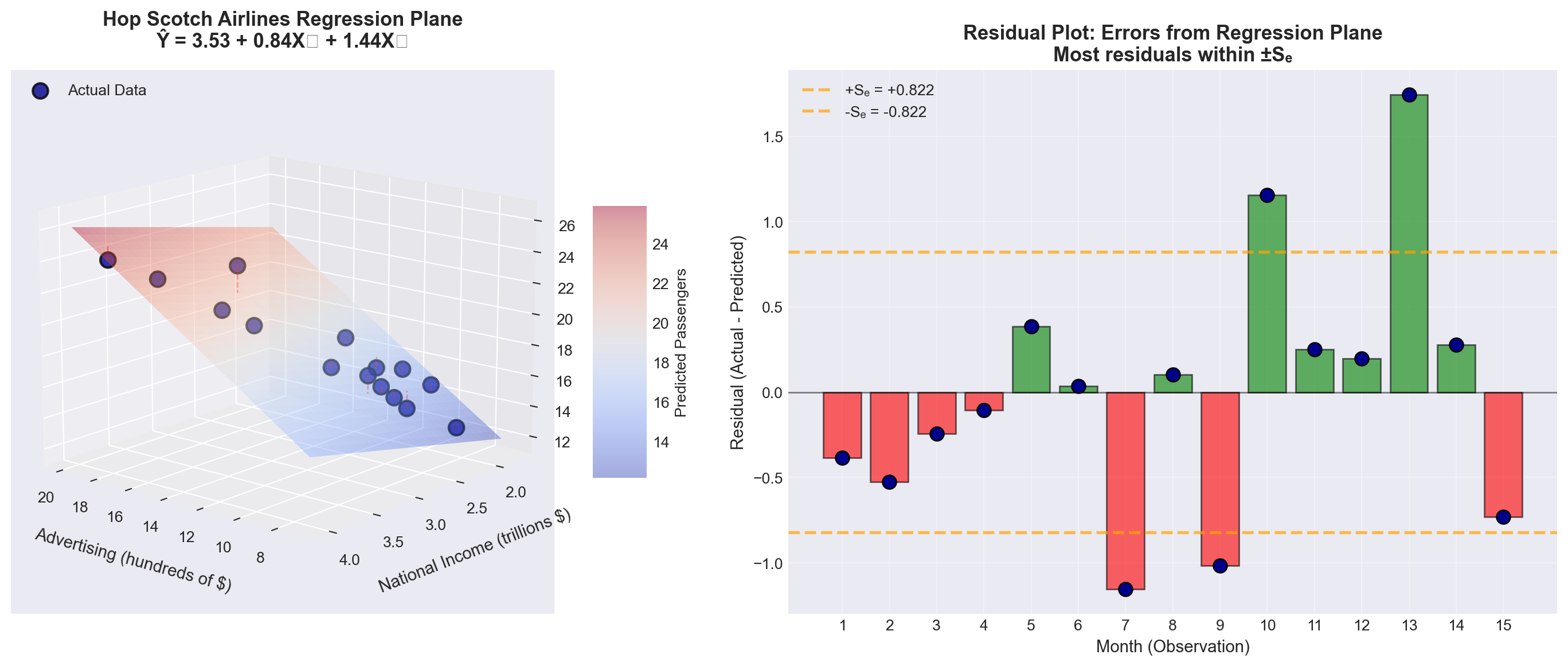

13.8.2 The Regression Plane Visualization

With two independent variables, we can visualize the model as a regression plane in three-dimensional space. Figure 13.2 shows this geometric interpretation:

Code

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Hop Scotch Airlines data from Table 12.1

data = {

'Month': range(1, 16),

'Passengers': [15, 17, 13, 23, 16, 21, 14, 20, 24, 17, 16, 18, 23, 15, 16],

'Advertising': [10, 12, 8, 17, 10, 15, 10, 14, 19, 10, 11, 13, 16, 10, 12],

'NationalIncome': [2.40, 2.72, 2.08, 3.68, 2.56, 3.36, 2.24, 3.20, 3.84, 2.72, 2.07, 2.33, 2.98, 1.94, 2.17]

}

df = pd.DataFrame(data)

# Regression coefficients (from Python output, Screen 12.1)

b0 = 3.5284

b1 = 0.8397

b2 = 1.4410

# Create figure with two subplots

fig = plt.figure(figsize=(15, 6))

# First subplot: 3D regression plane

ax1 = fig.add_subplot(121, projection='3d')

# Create mesh for regression plane

X1_mesh = np.linspace(df['Advertising'].min() - 1, df['Advertising'].max() + 1, 30)

X2_mesh = np.linspace(df['NationalIncome'].min() - 0.2, df['NationalIncome'].max() + 0.2, 30)

X1_grid, X2_grid = np.meshgrid(X1_mesh, X2_mesh)

Y_grid = b0 + b1*X1_grid + b2*X2_grid

# Plot the regression plane

surf = ax1.plot_surface(X1_grid, X2_grid, Y_grid, alpha=0.4,

cmap=cm.coolwarm, edgecolor='none')

# Plot actual data points

scatter = ax1.scatter(df['Advertising'], df['NationalIncome'], df['Passengers'],

c='darkblue', marker='o', s=100, alpha=0.8,

edgecolors='black', linewidth=1.5, label='Actual Data')

# Draw residuals (vertical lines from points to plane)

for i in range(len(df)):

Y_pred = b0 + b1*df['Advertising'].iloc[i] + b2*df['NationalIncome'].iloc[i]

ax1.plot([df['Advertising'].iloc[i], df['Advertising'].iloc[i]],

[df['NationalIncome'].iloc[i], df['NationalIncome'].iloc[i]],

[df['Passengers'].iloc[i], Y_pred],

'r--', alpha=0.4, linewidth=1)

ax1.set_xlabel('Advertising (hundreds of $)', fontsize=11, labelpad=10)

ax1.set_ylabel('National Income (trillions $)', fontsize=11, labelpad=10)

ax1.set_zlabel('Passengers (thousands)', fontsize=11, labelpad=10)

ax1.set_title('Hop Scotch Airlines Regression Plane\nŶ = 3.53 + 0.84X₁ + 1.44X₂',

fontsize=13, fontweight='bold', pad=15)

ax1.view_init(elev=15, azim=130)

ax1.legend(loc='upper left')

# Add colorbar

cbar1 = fig.colorbar(surf, ax=ax1, shrink=0.5, aspect=5)

cbar1.set_label('Predicted Passengers', fontsize=10)

# Second subplot: Residuals over time

ax2 = fig.add_subplot(122)

# Calculate residuals

df['Predicted'] = b0 + b1*df['Advertising'] + b2*df['NationalIncome']

df['Residual'] = df['Passengers'] - df['Predicted']

# Plot residuals

ax2.axhline(y=0, color='black', linestyle='-', linewidth=1, alpha=0.5)

ax2.bar(df['Month'], df['Residual'], color=['red' if x < 0 else 'green' for x in df['Residual']],

alpha=0.6, edgecolor='black', linewidth=1)

ax2.scatter(df['Month'], df['Residual'], c='darkblue', s=80, zorder=3,

edgecolors='black', linewidth=1)

# Add horizontal lines at ±Se

Se = 0.8217 # From Python output

ax2.axhline(y=Se, color='orange', linestyle='--', linewidth=2, alpha=0.7, label=f'+Sₑ = +{Se:.3f}')

ax2.axhline(y=-Se, color='orange', linestyle='--', linewidth=2, alpha=0.7, label=f'-Sₑ = -{Se:.3f}')

ax2.set_xlabel('Month (Observation)', fontsize=11)

ax2.set_ylabel('Residual (Actual - Predicted)', fontsize=11)

ax2.set_title('Residual Plot: Errors from Regression Plane\nMost residuals within ±Sₑ',

fontsize=13, fontweight='bold')

ax2.grid(True, alpha=0.3)

ax2.legend(loc='best')

ax2.set_xticks(df['Month'])

plt.tight_layout()

plt.show()

TipUnderstanding the Regression Plane

Left panel (3D visualization): - The colored surface is the regression plane: \hat{Y} = 3.53 + 0.84X_1 + 1.44X_2 - Blue points represent actual monthly passenger data - Red dashed lines show residuals (prediction errors) - The plane slopes upward in both directions (both coefficients are positive)

Right panel (Residual analysis): - Green bars = Months where model overestimated passengers - Red bars = Months where model underestimated passengers - Orange dashed lines = One standard error (\pm S_e) - Most residuals fall within \pm S_e, indicating good fit

Key insight: The regression plane represents the “best fit” surface that minimizes the sum of squared residuals \sum(Y_i - \hat{Y}_i)^2.

13.8.3 The Data: Hop Scotch Airlines Example

Table 13.1 shows the complete dataset for our analysis:

Code

import pandas as pd

# Create the data

data = {

'Observation\n(Month)': range(1, 16),

'Passengers (Y)\n(thousands)': [15, 17, 13, 23, 16, 21, 14, 20, 24, 17, 16, 18, 23, 15, 16],

'Advertising (X₁)\n($100s)': [10, 12, 8, 17, 10, 15, 10, 14, 19, 10, 11, 13, 16, 10, 12],

'National Income (X₂)\n($ trillions)': [2.40, 2.72, 2.08, 3.68, 2.56, 3.36, 2.24, 3.20, 3.84, 2.72, 2.07, 2.33, 2.98, 1.94, 2.17]

}

df = pd.DataFrame(data)

# Style the table

styled_df = df.style.set_properties(**{

'text-align': 'center',

'border': '1px solid black'

}).set_table_styles([

{'selector': 'th', 'props': [('background-color', '#e1f5ff'),

('color', 'black'),

('font-weight', 'bold'),

('text-align', 'center'),

('border', '1px solid black')]},

{'selector': 'td', 'props': [('border', '1px solid black')]}

]).hide(axis='index')

styled_df| Observation (Month) | Passengers (Y) (thousands) | Advertising (X₁) ($100s) | National Income (X₂) ($ trillions) |

|---|---|---|---|

| 1 | 15 | 10 | 2.400000 |

| 2 | 17 | 12 | 2.720000 |

| 3 | 13 | 8 | 2.080000 |

| 4 | 23 | 17 | 3.680000 |

| 5 | 16 | 10 | 2.560000 |

| 6 | 21 | 15 | 3.360000 |

| 7 | 14 | 10 | 2.240000 |

| 8 | 20 | 14 | 3.200000 |

| 9 | 24 | 19 | 3.840000 |

| 10 | 17 | 10 | 2.720000 |

| 11 | 16 | 11 | 2.070000 |

| 12 | 18 | 13 | 2.330000 |

| 13 | 23 | 16 | 2.980000 |

| 14 | 15 | 10 | 1.940000 |

| 15 | 16 | 12 | 2.170000 |

Observations about the data: - Sample size: n = 15 months - Advertising ranges from $800 to $1,900 (8 to 19 units) - National income ranges from $1.94 to $3.84 trillion - Passengers range from 13,000 to 24,000 (13 to 24 units) - We have k = 2 independent variables, so degrees of freedom = n - k - 1 = 15 - 2 - 1 = 12

13.8.4 Manual Calculation: A Cautionary Note

WarningWhy We Use Computers for Multiple Regression

Calculating a multiple regression model manually is extremely tedious and time-consuming. The procedure requires solving a system of k + 1 simultaneous equations with k + 1 unknowns.

For our Hop Scotch example with k = 2 variables: - We need to solve 3 equations with 3 unknowns (b_0, b_1, b_2) - The normal equations involve extensive matrix algebra - Manual calculation would take hours and be prone to arithmetic errors

Modern approach:

- We rely entirely on statistical software (Python, R, Python, Excel, SPSS, SAS, etc.) - Focus shifts to understanding and interpreting results rather than calculations - This allows us to concentrate on business insights and decision-making

For this reason, we will focus on understanding the fundamentals necessary to comprehend and interpret the multiple regression model, leaving the computational heavy lifting to the computer.

13.9 12.6 Computer Output and Model Interpretation

Table 13.2 shows the Python regression output for the Hop Scotch Airlines data:

Regression Analysis: PASS versus ADV, NI

The regression equation is

PASS = 3.53 + 0.840 ADV + 1.44 NI

Predictor Coef SE Coef T P VIF

Constant 3.5284 0.9994 3.53 0.004

ADV 0.8397 0.1419 5.92 0.000 4.1

NI 1.4410 0.7360 1.96 0.074 4.1

S = 0.8217 R-Sq = 95.3% R-Sq(adj) = 94.5%

Analysis of Variance

Source DF SS MS F P

Regression 2 163.632 81.816 121.18 0.000

Residual Error 12 8.102 0.675

Total 14 171.733

Source DF Seq SS

ADV 1 161.044

NI 1 2.58813.9.1 The Estimated Regression Equation

From the output, rounding coefficients for easier discussion:

\widehat{\text{Pass}} = 3.53 + 0.84 \times \text{Adv} + 1.44 \times \text{NI}

ImportantInterpreting the Partial Regression Coefficients

Intercept (b_0 = 3.53):

- When both advertising and national income equal zero, the model predicts 3,530 passengers - This value has limited practical meaning (baseline theoretical value)

Advertising Coefficient (b_1 = 0.84):

- For each additional unit of advertising ($100), passengers increase by 0.84 units (840 passengers) - Critical condition: This interpretation assumes national income remains constant - Business meaning: A $100 increase in advertising → 840 more passengers (holding economy constant)

National Income Coefficient (b_2 = 1.44):

- For each additional trillion dollars in national income, passengers increase by 1.44 units (1,440 passengers) - Critical condition: This interpretation assumes advertising remains constant - Business meaning: A $1 trillion increase in national income → 1,440 more passengers (holding advertising constant)

Example Prediction 12.1: What passenger volume can Hop Scotch expect if they spend $1,200 on advertising (X₁ = 12) when national income is $2.5 trillion (X₂ = 2.5)?

\begin{aligned} \widehat{\text{Pass}} &= 3.53 + 0.84(12) + 1.44(2.5) \\ &= 3.53 + 10.08 + 3.60 \\ &= 17.21 \text{ thousand passengers} \end{aligned}

Interpretation: Under these conditions, the model predicts approximately 17,210 passengers.

13.10 12.7 Evaluating the Multiple Regression Model

After estimating the model, we must evaluate its quality. Does it provide a satisfactory fit and explanation for the data? Several diagnostic tests help us make this determination.

13.10.1 A. The Standard Error of Estimation (S_e)

Just as in simple regression, the standard error of estimation measures the goodness of fit. It quantifies the typical distance of data points from the regression plane.

NoteStandard Error of Estimation (Multiple Regression)

S_e = \sqrt{\frac{\sum(Y_i - \hat{Y}_i)^2}{n - k - 1}}

Where:

- \sum(Y_i - \hat{Y}_i)^2 = Sum of squared residuals (SSE) - n = Number of observations - k = Number of independent variables - n - k - 1 = Degrees of freedom

Interpretation:

- Measures dispersion of actual values around the regression plane - Smaller S_e → Better fit → More precise predictions - Has the same units as the dependent variable Y

Table 13.3 shows the detailed calculation:

Code

import pandas as pd

import numpy as np

# Hop Scotch data

data = {

'Month': range(1, 16),

'Y (Actual)': [15, 17, 13, 23, 16, 21, 14, 20, 24, 17, 16, 18, 23, 15, 16],

'Advertising': [10, 12, 8, 17, 10, 15, 10, 14, 19, 10, 11, 13, 16, 10, 12],

'NationalIncome': [2.40, 2.72, 2.08, 3.68, 2.56, 3.36, 2.24, 3.20, 3.84, 2.72, 2.07, 2.33, 2.98, 1.94, 2.17]

}

df = pd.DataFrame(data)

# Calculate predictions

b0, b1, b2 = 3.5284, 0.8397, 1.4410

df['Ŷ (Predicted)'] = b0 + b1*df['Advertising'] + b2*df['NationalIncome']

df['Residual (Y - Ŷ)'] = df['Y (Actual)'] - df['Ŷ (Predicted)']

df['(Y - Ŷ)²'] = df['Residual (Y - Ŷ)']**2

# Format for display

display_df = df[['Month', 'Y (Actual)', 'Ŷ (Predicted)', 'Residual (Y - Ŷ)', '(Y - Ŷ)²']].copy()

display_df['Ŷ (Predicted)'] = display_df['Ŷ (Predicted)'].round(4)

display_df['Residual (Y - Ŷ)'] = display_df['Residual (Y - Ŷ)'].round(5)

display_df['(Y - Ŷ)²'] = display_df['(Y - Ŷ)²'].round(5)

# Add totals row

totals = pd.DataFrame({

'Month': ['TOTAL'],

'Y (Actual)': [df['Y (Actual)'].sum()],

'Ŷ (Predicted)': [df['Ŷ (Predicted)'].sum()],

'Residual (Y - Ŷ)': [df['Residual (Y - Ŷ)'].sum()],

'(Y - Ŷ)²': [df['(Y - Ŷ)²'].sum()]

})

display_df = pd.concat([display_df, totals], ignore_index=True)

# Style the table

styled = display_df.style.set_properties(**{

'text-align': 'center',

'border': '1px solid black'

}).set_table_styles([

{'selector': 'th', 'props': [('background-color', '#fff4e1'),

('font-weight', 'bold'),

('text-align', 'center'),

('border', '1px solid black')]},

{'selector': 'td', 'props': [('border', '1px solid black')]},

{'selector': 'tr:last-child', 'props': [('background-color', '#ffe1e1'),

('font-weight', 'bold')]}

]).hide(axis='index').format({

'Ŷ (Predicted)': '{:.4f}',

'Residual (Y - Ŷ)': '{:.5f}',

'(Y - Ŷ)²': '{:.5f}'

})

styled| Month | Y (Actual) | Ŷ (Predicted) | Residual (Y - Ŷ) | (Y - Ŷ)² |

|---|---|---|---|---|

| 1 | 15 | 15.3838 | -0.38380 | 0.14730 |

| 2 | 17 | 17.5243 | -0.52432 | 0.27491 |

| 3 | 13 | 13.2433 | -0.24328 | 0.05919 |

| 4 | 23 | 23.1062 | -0.10618 | 0.01127 |

| 5 | 16 | 15.6144 | 0.38564 | 0.14872 |

| 6 | 21 | 20.9657 | 0.03434 | 0.00118 |

| 7 | 14 | 15.1532 | -1.15324 | 1.32996 |

| 8 | 20 | 19.8954 | 0.10460 | 0.01094 |

| 9 | 24 | 25.0161 | -1.01614 | 1.03254 |

| 10 | 17 | 15.8449 | 1.15508 | 1.33421 |

| 11 | 16 | 15.7480 | 0.25203 | 0.06352 |

| 12 | 18 | 17.8020 | 0.19797 | 0.03919 |

| 13 | 23 | 21.2578 | 1.74222 | 3.03533 |

| 14 | 15 | 14.7209 | 0.27906 | 0.07787 |

| 15 | 16 | 16.7318 | -0.73177 | 0.53549 |

| TOTAL | 268 | 268.0078 | -0.00779 | 8.10163 |

Calculating the standard error:

S_e = \sqrt{\frac{8.1016}{15 - 2 - 1}} = \sqrt{\frac{8.1016}{12}} = \sqrt{0.6751} = 0.8217

From Python output: S = 0.8217 ✓ (Our calculation matches!)

TipComparing Simple vs. Multiple Regression

Simple regression (Chapter 11):

- Model: \hat{Y} = 4.39 + 1.08X_1 (advertising only) - Standard error: S_e = 0.907

Multiple regression (current):

- Model: \hat{Y} = 3.53 + 0.84X_1 + 1.44X_2 (advertising + national income) - Standard error: S_e = 0.8217

Improvement: The standard error decreased from 0.907 to 0.822 by adding national income to the model. This represents a 9.4% reduction in prediction error—a meaningful improvement!

Business interpretation:

On average, the actual number of passengers deviates from the predicted number by approximately 822 passengers. This is our typical prediction error.

[Stage 2 continues with Sections 12.8-12.10 covering:*

- Coefficient of multiple determination (R²)

- Adjusted R²

- ANOVA F-test

- Individual t-tests for coefficients

*- Section exercises]

13.11 Section Exercises

12.11 Using the Hop Scotch Airlines data:

a. Verify the calculation of S_e = 0.8217 using the residuals from Table 13.3

b. Calculate the residual for Month 13 manually and compare to the table value

c. What percentage of residuals fall within \pm S_e?

12.12 Interpret the following regression output:

SALES = 15.2 + 2.3 PRICE + 0.85 INCOME

S = 3.45 R-Sq = 78.2% R-Sq(adj) = 76.8%- What does the coefficient 2.3 for PRICE mean?

- Does the positive coefficient for PRICE make economic sense? Explain

- What is the typical prediction error for this model?

12.13 A real estate model produces: \text{Price} = 45,000 + 120 \times \text{SqFt} + 18,000 \times \text{Bedrooms} with S_e = 15,000.

- Predict the price of a 2,000 sq ft house with 3 bedrooms

- What does S_e = 15,000 tell you about prediction accuracy?

- Construct an approximate 68% prediction interval for your answer in part (a)

12.14 True or False (explain):

a. A smaller standard error always means a better model

b. The standard error has the same units as the dependent variable

c. Adding more variables will always decrease the standard error

d. If S_e = 0, the model perfectly fits all data points

12.15 Calculate the standard error for this small dataset where the model is \hat{Y} = 10 + 2X_1 + 3X_2:

| Y | X₁ | X₂ | Ŷ |

|---|---|---|---|

| 20 | 2 | 1 | 19 |

| 25 | 3 | 2 | 22 |

| 30 | 4 | 3 | 29 |

| 35 | 5 | 3 | 31 |

| 40 | 6 | 4 | 40 |

Key Terms Introduced: - Regression plane - Partial regression coefficients - Standard error of estimation (multiple regression) - Residual analysis - Sum of squared errors (SSE)

Just as with simple regression, the coefficient of multiple determination serves as a crucial measure of goodness of fit. For convenience, the term “multiple” is often omitted when context makes it clear, and we simply refer to it as the coefficient of determination—the same term used for simple regression models.

The interpretation remains consistent across both model types: R^2 represents the proportion of variation in Y that is explained by all the independent variables in the model.

NoteCoefficient of Multiple Determination

Definition: R^2 measures the strength of the relationship between Y and the independent variables collectively.

Formula:

R^2 = \frac{SCR}{SCT} = \frac{\text{Sum of Squares Regression}}{\text{Sum of Squares Total}}

Alternatively:

R^2 = 1 - \frac{SCE}{SCT} = 1 - \frac{\text{Sum of Squares Error}}{\text{Sum of Squares Total}}

Where: - SCT = \sum(Y_i - \bar{Y})^2 = Total variation in Y - SCR = \sum(\hat{Y}_i - \bar{Y})^2 = Variation explained by the regression - SCE = \sum(Y_i - \hat{Y}_i)^2 = Unexplained variation (error) - Fundamental relationship: SCT = SCR + SCE

Properties: - Always falls between 0 and 1: 0 \leq R^2 \leq 1 - Expressed as a percentage (multiply by 100) - Higher values indicate better explanatory power - R^2 = 0: Model explains nothing (worthless) - R^2 = 1: Model explains everything (perfect fit)

Important notation distinction: - Simple regression: Use lowercase r^2 - Multiple regression: Use uppercase R^2

This helps distinguish between models with one versus multiple independent variables.

13.11.1 Calculating R^2 for Hop Scotch Airlines

From the Python output (Table 13.2 in Section 12.6), we find:

- SCR = 163.632 (Regression sum of squares)

- SCT = 171.733 (Total sum of squares)

Therefore:

\begin{aligned} R^2 &= \frac{SCR}{SCT} \\ &= \frac{163.632}{171.733} \\ &= 0.953 \end{aligned}

From Python: R-Sq = 95.3% ✓

ImportantInterpreting R^2 = 95.3\% for Hop Scotch

What it means:

95.3% of the variation in the number of passengers carried by Hop Scotch Airlines is explained by the combined effects of advertising expenditure and national income.

What it doesn’t mean: - It does NOT mean 95.3% of predictions are accurate - It does NOT mean there’s a 95.3% probability of correct prediction - It does NOT prove causation (correlation ≠ causation)

Business significance:

This is an excellent result! The model explains almost all the variation in passenger volume, leaving only 4.7% unexplained.

13.11.2 Improvement Over Simple Regression

Let’s compare the explanatory power:

Simple regression (Chapter 11):

- Model: Passengers = f(Advertising only) - r^2 = 0.937 or 93.7%

Multiple regression (current):

- Model: Passengers = f(Advertising, National Income) - R^2 = 0.953 or 95.3%

Gain from adding National Income: 95.3\% - 93.7\% = 1.6 percentage points

TipWas Adding National Income Worth It?

The question: National income only added 1.6% to explanatory power. Is this meaningful?

Considerations: 1. Absolute improvement: Small (1.6%) 2. Relative improvement: Reduced unexplained variation from 6.3% to 4.7% (a 25% reduction!) 3. Statistical significance: We’ll test this with t-tests (coming up) 4. Theoretical justification: Economic theory strongly supports income as a determinant of demand 5. Multicollinearity: High correlation between advertising and income (we’ll examine this)

Conclusion: The marginal benefit is modest but potentially valuable, especially if income data is readily available and doesn’t introduce serious multicollinearity.

13.11.3 C. The Adjusted Coefficient of Determination (\bar{R}^2)

While R^2 is the most commonly reported statistic in regression analysis, it has a serious flaw: it can be artificially inflated by adding variables—any variables, even irrelevant ones.

13.11.3.1 The Problem with R^2

WarningThe R^2 Inflation Problem

An unscrupulous (or careless) analyst could:

- Start with a basic model

- Add random, logically irrelevant variables

- Watch R^2 increase with each addition

- Report an impressive-looking R^2 near 100%

Example: Hop Scotch could “inflate” their R^2 by adding: - Trout caught off the Florida coast - Wheat production in Kansas

- Average temperature in Antarctica - Number of weddings in Las Vegas

Even though these variables have nothing to do with airline passengers, each would likely show some tiny, spurious correlation. Adding enough such variables could push R^2 toward 100%.

Why this happens:

R^2 cannot decrease when you add variables. At worst, it stays the same; usually it increases slightly, even for nonsense variables.

The result:

A model that looks statistically impressive but: - Violates economic/business theory (specification bias) - Makes no logical sense - Produces unreliable predictions - Misleads decision-makers

13.11.3.2 The Solution: Adjusted R^2

To prevent this abuse, statisticians developed the adjusted coefficient of determination, denoted \bar{R}^2 (read as “R-bar squared”). This statistic adjusts for the number of degrees of freedom.

NoteAdjusted Coefficient of Determination

\bar{R}^2 = 1 - \frac{SCE/(n-k-1)}{SCT/(n-1)}

Computational formula (easier):

\bar{R}^2 = 1 - (1 - R^2)\frac{n-1}{n-k-1}

Where: - n = Number of observations - k = Number of independent variables - n - k - 1 = Degrees of freedom for error - n - 1 = Degrees of freedom for total variation

Key properties: - \bar{R}^2 \leq R^2 (adjusted is always equal or smaller) - \bar{R}^2 can be negative (though rare) - \bar{R}^2 can decrease when you add a weak variable - Penalizes models for including unnecessary variables

The adjustment mechanism:

The formula divides SCE and SCT by their respective degrees of freedom. Adding a variable: - Increases k (more variables) - Decreases n - k - 1 (fewer degrees of freedom) - This increases the denominator penalty

If the variable doesn’t contribute enough explanatory power to justify the loss of a degree of freedom, \bar{R}^2 will decrease.

13.11.4 Calculating \bar{R}^2 for Hop Scotch

Given: - R^2 = 0.953 - n = 15 observations - k = 2 independent variables

\begin{aligned} \bar{R}^2 &= 1 - (1 - R^2)\frac{n-1}{n-k-1} \\ &= 1 - (1 - 0.953)\frac{15-1}{15-2-1} \\ &= 1 - (0.047)\frac{14}{12} \\ &= 1 - 0.0548 \\ &= 0.945 \end{aligned}

From Python: R-Sq(adj) = 94.5% ✓

Interpretation:

After adjusting for degrees of freedom, the model explains 94.5% of the variation in passengers—only 0.8 percentage points less than the unadjusted R^2.

TipWhat \bar{R}^2 Tells Us

The small difference between R^2 = 95.3\% and \bar{R}^2 = 94.5\% suggests:

- Both variables contribute meaningfully (if they didn’t, the gap would be larger)

- Sample size is adequate relative to the number of variables

- The model is appropriately specified (not overloaded with variables)

Rule of thumb:

- If R^2 - \bar{R}^2 < 0.05: Model is likely well-specified - If R^2 - \bar{R}^2 > 0.10: Too many variables for the sample size; consider removing some

Alternative interpretation:

\bar{R}^2 combines two important model quality measures: - CME (Mean Square Error): CME = SCE/(n-k-1) - R^2 (Coefficient of Determination)

Thus, \bar{R}^2 is a balanced measure that considers both fit and parsimony (simplicity).

13.11.5 D. Evaluating the Model as a Whole: ANOVA F-Test

After constructing a multiple regression model, the first critical question is:

“Does this model have any explanatory value at all?”

This is answered using Analysis of Variance (ANOVA), which tests whether at least one independent variable has a relationship with the dependent variable.

13.11.5.1 The Hypothesis Test

ImportantANOVA Test for Overall Model Significance

Hypotheses:

H_0: \beta_1 = \beta_2 = \beta_3 = \cdots = \beta_k = 0 H_A: \text{At least one } \beta_j \neq 0

What the null hypothesis means:

ALL regression coefficients are zero, meaning NONE of the independent variables have any relationship with Y. The model is completely useless.

What the alternative means:

AT LEAST ONE coefficient is non-zero, meaning AT LEAST ONE variable has a relationship with Y. The model has some value.

Decision implications: - Fail to reject H_0: The model is worthless; no variables explain Y - Reject H_0: The model has value; at least one variable explains part of Y

Important note: This test does NOT tell us: - Which variables are significant (that requires individual t-tests) - How many variables are significant - How strong the relationships are

It only tells us whether the model as a whole is better than nothing.

13.11.5.2 The ANOVA Table Structure

The general format for a multiple regression ANOVA table:

| Source of Variation | Sum of Squares | Degrees of Freedom | Mean Square | F-ratio |

|---|---|---|---|---|

| Regression | SCR | k | CMR = \frac{SCR}{k} | F = \frac{CMR}{CME} |

| Error | SCE | n-k-1 | CME = \frac{SCE}{n-k-1} | |

| Total | SCT | n-1 |

Key formulas (same as simple regression):

SCT = \sum(Y_i - \bar{Y})^2 \quad \text{(Total variation)}

SCR = \sum(\hat{Y}_i - \bar{Y})^2 \quad \text{(Explained variation)}

SCE = \sum(Y_i - \hat{Y}_i)^2 \quad \text{(Unexplained variation)}

Degrees of freedom: - Regression: k (number of independent variables) - Error: n - k - 1 (observations minus parameters estimated) - Total: n - 1 (observations minus 1)

13.11.5.3 ANOVA Results for Hop Scotch Airlines

From the Python output:

| Source | DF | SS | MS | F | p-value |

|---|---|---|---|---|---|

| Regression | 2 | 163.632 | 81.816 | 121.18 | 0.000 |

| Error | 12 | 8.102 | 0.675 | ||

| Total | 14 | 171.733 |

Calculations verified: - CMR = SCR/k = 163.632/2 = 81.816 ✓ - CME = SCE/(n-k-1) = 8.102/12 = 0.675 ✓ - F = CMR/CME = 81.816/0.675 = 121.18 ✓

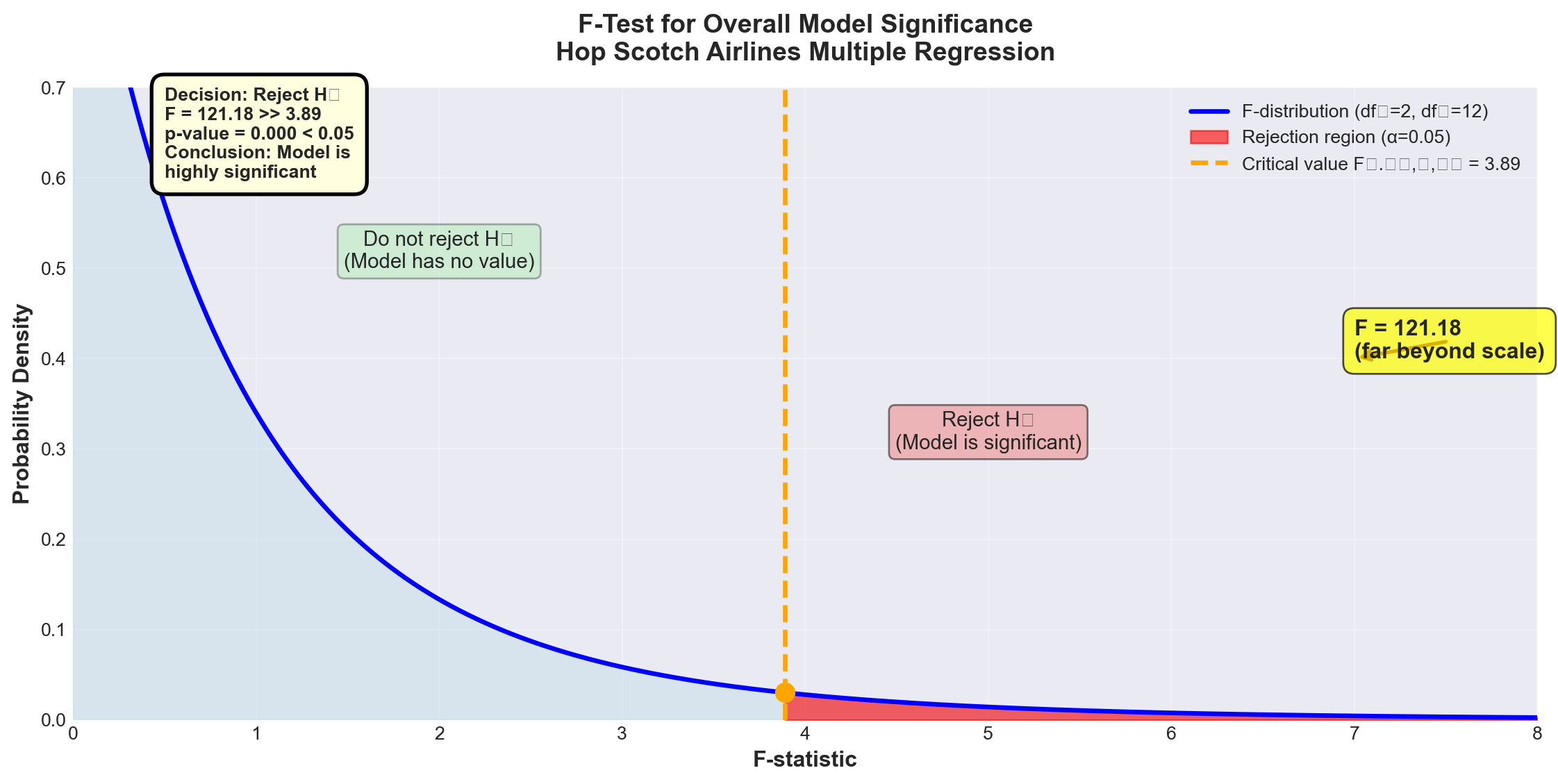

13.11.5.4 Conducting the F-Test

Test setup: - H_0: \beta_1 = \beta_2 = 0 (both advertising and national income have no effect) - H_A: At least one \beta \neq 0 (at least one variable matters) - \alpha = 0.05 (5% significance level) - Degrees of freedom: df_1 = 2, df_2 = 12

Critical value from F-table:

F_{0.05, 2, 12} = 3.89

Decision rule:

Reject H_0 if F_{calculated} > 3.89

Code

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Create figure

fig, ax = plt.subplots(figsize=(12, 6))

# F-distribution parameters

df1, df2 = 2, 12

x = np.linspace(0, 8, 1000)

y = stats.f.pdf(x, df1, df2)

# Plot the F-distribution

ax.plot(x, y, 'b-', linewidth=2.5, label=f'F-distribution (df₁={df1}, df₂={df2})')

ax.fill_between(x, 0, y, alpha=0.3, color='lightblue')

# Critical value

F_critical = 3.89

F_calculated = 121.18

# Shade rejection region

x_reject = x[x >= F_critical]

y_reject = stats.f.pdf(x_reject, df1, df2)

ax.fill_between(x_reject, 0, y_reject, alpha=0.6, color='red',

label=f'Rejection region (α=0.05)')

# Mark critical value

ax.axvline(F_critical, color='orange', linestyle='--', linewidth=2.5,

label=f'Critical value F₀.₀₅,₂,₁₂ = {F_critical}')

ax.plot(F_critical, stats.f.pdf(F_critical, df1, df2), 'o',

color='orange', markersize=10)

# Mark calculated F (off the chart, so show with annotation)

ax.annotate(f'F = {F_calculated:.2f}\n(far beyond scale)',

xy=(7, 0.4), fontsize=12, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.5', facecolor='yellow', alpha=0.7),

arrowprops=dict(arrowstyle='->', lw=2, color='darkred'))

# Add text annotations

ax.text(2, 0.5, 'Do not reject H₀\n(Model has no value)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightgreen', alpha=0.3))

ax.text(5, 0.3, 'Reject H₀\n(Model is significant)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightcoral', alpha=0.5))

# Labels and formatting

ax.set_xlabel('F-statistic', fontsize=12, fontweight='bold')

ax.set_ylabel('Probability Density', fontsize=12, fontweight='bold')

ax.set_title('F-Test for Overall Model Significance\nHop Scotch Airlines Multiple Regression',

fontsize=14, fontweight='bold', pad=15)

ax.set_xlim(0, 8)

ax.set_ylim(0, 0.7)

ax.legend(loc='upper right', fontsize=10, framealpha=0.9)

ax.grid(True, alpha=0.3)

# Add decision box

decision_text = (

'Decision: Reject H₀\n'

'F = 121.18 >> 3.89\n'

'p-value = 0.000 < 0.05\n'

'Conclusion: Model is\n'

'highly significant'

)

ax.text(0.5, 0.6, decision_text, fontsize=10, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.7', facecolor='lightyellow',

edgecolor='black', linewidth=2))

plt.tight_layout()

plt.show()

ImportantTest Results and Conclusion

Calculated F-statistic: F = 121.18

Critical value: F_{0.05, 2, 12} = 3.89

p-value: p = 0.000

Decision: Since F = 121.18 > 3.89, we reject the null hypothesis at the 5% significance level.

Conclusion:

At least one of the independent variables (advertising or national income) has a statistically significant linear relationship with the number of passengers. The model as a whole is highly significant.

Business interpretation:

The regression model has substantial explanatory value. We can be extremely confident (p < 0.001) that advertising and/or national income genuinely affect passenger volume—this is not just random chance.

Note on the p-value:

The p-value of 0.000 doesn’t mean exactly zero—it means p < 0.0005, which rounds to 0.000 in the output. This represents overwhelming evidence against the null hypothesis.

13.11.6 E. Testing Individual Regression Coefficients

The ANOVA F-test told us the model as a whole is significant, but it didn’t tell us which variables are significant. The next logical step is to test each coefficient individually.

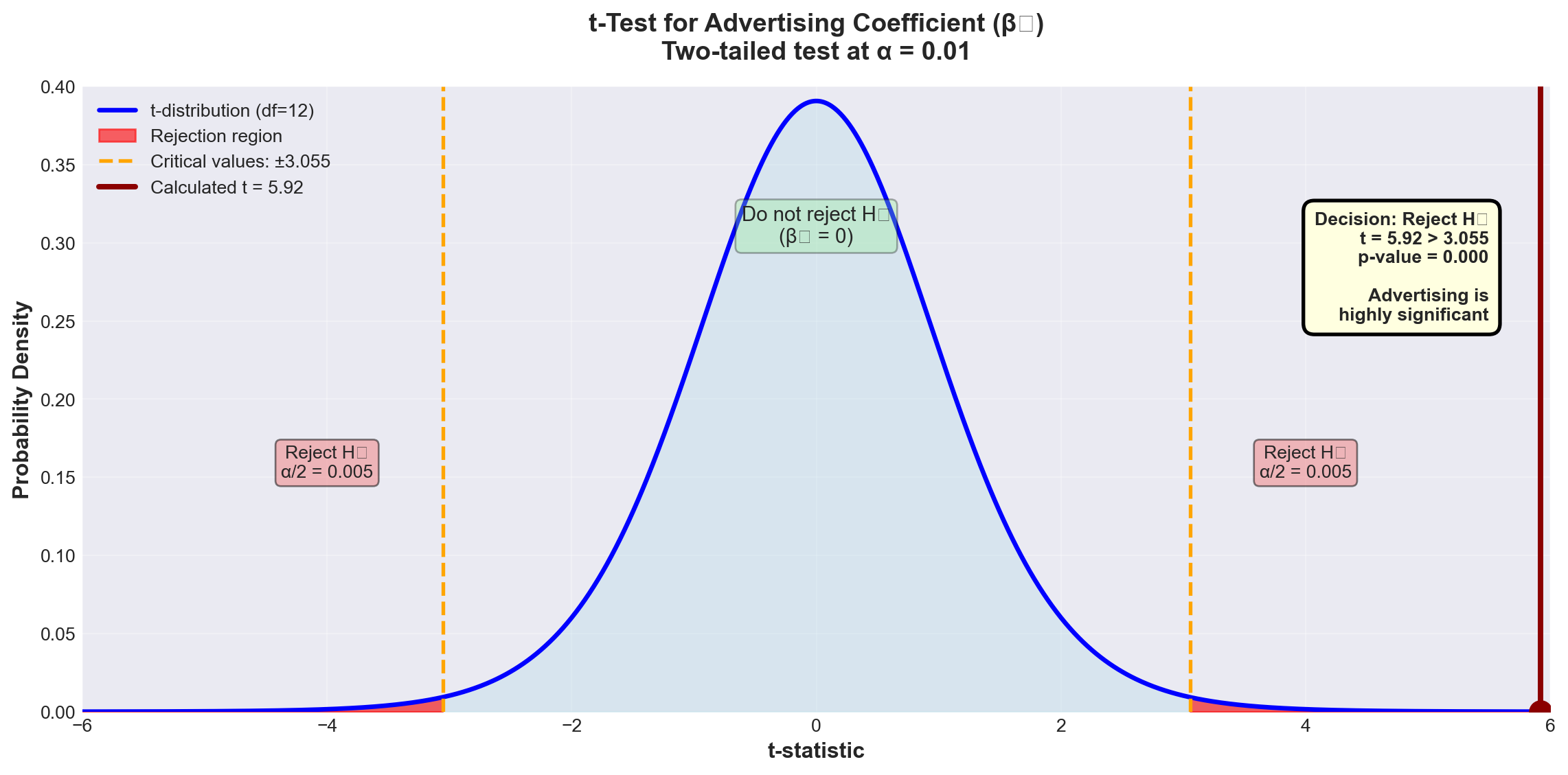

13.11.6.1 Testing the Advertising Coefficient (\beta_1)

NoteHypothesis Test for \beta_1 (Advertising)

Hypotheses: H_0: \beta_1 = 0 H_A: \beta_1 \neq 0

What the null hypothesis means:

Advertising has no effect on passengers, given that national income is already in the model.

Critical insight:

This is NOT the same as testing advertising alone (which gave t = 13.995 in Chapter 11). This tests advertising’s additional contribution after accounting for national income.

Test statistic:

t = \frac{b_1 - \beta_1}{S_{b_1}}

With n - k - 1 degrees of freedom.

From Python output: - b_1 = 0.8397 - S_{b_1} = 0.1419 (standard error of b_1) - Under H_0: \beta_1 = 0

t = \frac{0.8397 - 0}{0.1419} = 5.92

Test at \alpha = 0.01 (1% level): - Degrees of freedom: n - k - 1 = 15 - 2 - 1 = 12 - Critical value: t_{0.01, 12} = \pm 3.055 (two-tailed)

Decision rule:

Reject H_0 if |t| > 3.055

Code

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Create figure

fig, ax = plt.subplots(figsize=(12, 6))

# t-distribution parameters

df = 12

x = np.linspace(-6, 6, 1000)

y = stats.t.pdf(x, df)

# Plot the t-distribution

ax.plot(x, y, 'b-', linewidth=2.5, label=f't-distribution (df={df})')

ax.fill_between(x, 0, y, alpha=0.3, color='lightblue')

# Critical values

t_critical = 3.055

t_calculated = 5.92

# Shade rejection regions

x_left = x[x <= -t_critical]

y_left = stats.t.pdf(x_left, df)

ax.fill_between(x_left, 0, y_left, alpha=0.6, color='red', label='Rejection region')

x_right = x[x >= t_critical]

y_right = stats.t.pdf(x_right, df)

ax.fill_between(x_right, 0, y_right, alpha=0.6, color='red')

# Mark critical values

ax.axvline(-t_critical, color='orange', linestyle='--', linewidth=2,

label=f'Critical values: ±{t_critical}')

ax.axvline(t_critical, color='orange', linestyle='--', linewidth=2)

# Mark calculated t-value

ax.axvline(t_calculated, color='darkred', linestyle='-', linewidth=3,

label=f'Calculated t = {t_calculated}')

ax.plot(t_calculated, stats.t.pdf(t_calculated, df), 'o',

color='darkred', markersize=12)

# Add annotations

ax.text(0, 0.3, 'Do not reject H₀\n(β₁ = 0)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightgreen', alpha=0.3))

ax.text(-4, 0.15, 'Reject H₀\nα/2 = 0.005',

fontsize=10, ha='center',

bbox=dict(boxstyle='round', facecolor='lightcoral', alpha=0.5))

ax.text(4, 0.15, 'Reject H₀\nα/2 = 0.005',

fontsize=10, ha='center',

bbox=dict(boxstyle='round', facecolor='lightcoral', alpha=0.5))

# Labels and formatting

ax.set_xlabel('t-statistic', fontsize=12, fontweight='bold')

ax.set_ylabel('Probability Density', fontsize=12, fontweight='bold')

ax.set_title('t-Test for Advertising Coefficient (β₁)\nTwo-tailed test at α = 0.01',

fontsize=14, fontweight='bold', pad=15)

ax.set_xlim(-6, 6)

ax.set_ylim(0, 0.4)

ax.legend(loc='upper left', fontsize=10, framealpha=0.9)

ax.grid(True, alpha=0.3)

# Add decision box

decision_text = (

'Decision: Reject H₀\n'

't = 5.92 > 3.055\n'

'p-value = 0.000\n\n'

'Advertising is\n'

'highly significant'

)

ax.text(5.5, 0.32, decision_text, fontsize=10, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.6', facecolor='lightyellow',

edgecolor='black', linewidth=2),

verticalalignment='top', horizontalalignment='right')

plt.tight_layout()

plt.show()

ImportantResults for Advertising Coefficient

Decision: Since t = 5.92 > 3.055, we reject H_0 at the 1% significance level.

Conclusion:

Advertising contributes significantly to explaining passenger volume, even after national income is already included in the model.

p-value = 0.000 confirms this: We could lower \alpha all the way to 0.000 and still reject H_0.

Business interpretation:

Advertising expenditure has a genuine, statistically significant effect on passenger numbers, independent of economic conditions (national income). This justifies continued investment in advertising.

Why is the t-value different from Chapter 11?

In Chapter 11, when advertising was the ONLY variable, we found t = 13.995. Now, with national income in the model, t = 5.92 for advertising.

Explanation:

- Chapter 11 t-value (13.995): Advertising’s total effect on passengers - Chapter 12 t-value (5.92): Advertising’s additional contribution beyond what national income already explains

The difference reflects the fact that advertising and national income are correlated (we’ll examine this multicollinearity issue in the next stage).

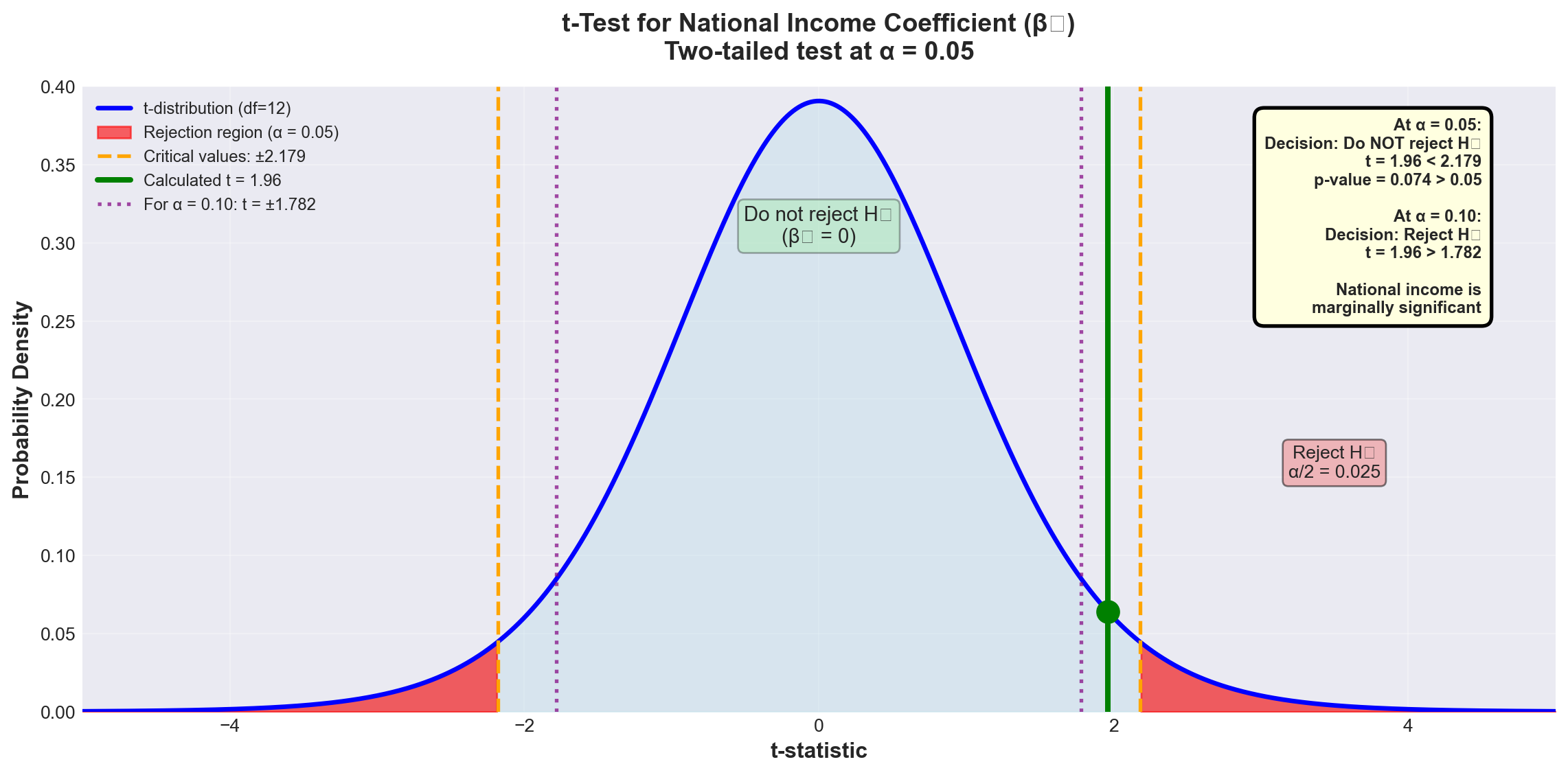

13.11.6.2 Testing the National Income Coefficient (\beta_2)

NoteHypothesis Test for \beta_2 (National Income)

Hypotheses: H_0: \beta_2 = 0 H_A: \beta_2 \neq 0

What it tests:

Does national income contribute to explaining passengers, given that advertising is already in the model?

From Python output: - b_2 = 1.4410 - S_{b_2} = 0.7360

t = \frac{1.4410 - 0}{0.7360} = 1.96

Test at \alpha = 0.05 (5% level): - Critical value: t_{0.05, 12} = \pm 2.179

Decision rule:

Reject H_0 if |t| > 2.179

Code

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Create figure

fig, ax = plt.subplots(figsize=(12, 6))

# t-distribution parameters

df = 12

x = np.linspace(-5, 5, 1000)

y = stats.t.pdf(x, df)

# Plot the t-distribution

ax.plot(x, y, 'b-', linewidth=2.5, label=f't-distribution (df={df})')

ax.fill_between(x, 0, y, alpha=0.3, color='lightblue')

# Critical values

t_critical = 2.179

t_calculated = 1.96

# Shade rejection regions

x_left = x[x <= -t_critical]

y_left = stats.t.pdf(x_left, df)

ax.fill_between(x_left, 0, y_left, alpha=0.6, color='red', label='Rejection region (α = 0.05)')

x_right = x[x >= t_critical]

y_right = stats.t.pdf(x_right, df)

ax.fill_between(x_right, 0, y_right, alpha=0.6, color='red')

# Mark critical values

ax.axvline(-t_critical, color='orange', linestyle='--', linewidth=2,

label=f'Critical values: ±{t_critical}')

ax.axvline(t_critical, color='orange', linestyle='--', linewidth=2)

# Mark calculated t-value

ax.axvline(t_calculated, color='green', linestyle='-', linewidth=3,

label=f'Calculated t = {t_calculated}')

ax.plot(t_calculated, stats.t.pdf(t_calculated, df), 'o',

color='green', markersize=12)

# Add shaded region for α = 0.10 test (wider)

t_critical_10 = 1.782

ax.axvline(t_critical_10, color='purple', linestyle=':', linewidth=2, alpha=0.7,

label=f'For α = 0.10: t = ±{t_critical_10}')

ax.axvline(-t_critical_10, color='purple', linestyle=':', linewidth=2, alpha=0.7)

# Add annotations

ax.text(0, 0.3, 'Do not reject H₀\n(β₂ = 0)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightgreen', alpha=0.3))

ax.text(3.5, 0.15, 'Reject H₀\nα/2 = 0.025',

fontsize=10, ha='center',

bbox=dict(boxstyle='round', facecolor='lightcoral', alpha=0.5))

# Labels and formatting

ax.set_xlabel('t-statistic', fontsize=12, fontweight='bold')

ax.set_ylabel('Probability Density', fontsize=12, fontweight='bold')

ax.set_title('t-Test for National Income Coefficient (β₂)\nTwo-tailed test at α = 0.05',

fontsize=14, fontweight='bold', pad=15)

ax.set_xlim(-5, 5)

ax.set_ylim(0, 0.4)

ax.legend(loc='upper left', fontsize=9, framealpha=0.9)

ax.grid(True, alpha=0.3)

# Add decision box

decision_text = (

'At α = 0.05:\n'

'Decision: Do NOT reject H₀\n'

't = 1.96 < 2.179\n'

'p-value = 0.074 > 0.05\n\n'

'At α = 0.10:\n'

'Decision: Reject H₀\n'

't = 1.96 > 1.782\n\n'

'National income is\n'

'marginally significant'

)

ax.text(4.5, 0.38, decision_text, fontsize=9, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.6', facecolor='lightyellow',

edgecolor='black', linewidth=2),

verticalalignment='top', horizontalalignment='right')

plt.tight_layout()

plt.show()

WarningResults for National Income Coefficient

At \alpha = 0.05:

Since t = 1.96 < 2.179, we fail to reject H_0.

Conclusion at 5% level:

We cannot conclude that national income significantly contributes to explaining passengers, given that advertising is already in the model.

However, examining the p-value:

p = 0.074 means we could lower \alpha to 7.4% and reject H_0.

At \alpha = 0.10:

Critical value: t_{0.10, 12} = \pm 1.782

Since t = 1.96 > 1.782, we reject H_0 at the 10% level.

Business interpretation:

National income shows marginal significance. While not significant at the conventional 5% level, it contributes at the 10% level. The decision to keep it in the model depends on: - Business theory (income should matter for air travel demand) - Cost of collecting the data - Multicollinearity concerns (coming in next stage) - Management’s tolerance for Type I error risk

13.12 Section Exercises

12.16 Using the ANOVA results for Hop Scotch Airlines:

a. Calculate the F-ratio manually and verify it equals 121.18

b. What would the conclusion be at \alpha = 0.01? At \alpha = 0.001?

c. Explain in business terms what rejecting H_0 means

12.17 For a regression with n = 25, k = 3, R^2 = 0.78:

a. Calculate \bar{R}^2

b. Is the difference between R^2 and \bar{R}^2 concerning? Why or why not?

12.18 Interpret the following regression results:

SALES = 50 + 3.2 PRICE + 0.85 INCOME + 1.5 COMPETITORS

Coef SE Coef T P

Constant 50.00 12.50 4.00 0.001

PRICE 3.20 0.45 7.11 0.000

INCOME 0.85 0.22 3.86 0.002

COMPETITORS 1.50 1.20 1.25 0.225

S = 5.2 R-Sq = 82.5% R-Sq(adj) = 80.1% F = 34.6 p = 0.000- Is the overall model significant at \alpha = 0.01?

- Which variables are significant at \alpha = 0.05?

- Does the positive coefficient for PRICE make economic sense? Explain

- Should COMPETITORS be removed from the model? Justify your answer

12.19 Given: SCT = 450, SCR = 360, n = 20, k = 4

a. Calculate R^2 and \bar{R}^2

b. Calculate the F-statistic

c. Is the model significant at \alpha = 0.05?

12.20 True or False (explain each):

a. R^2 can never decrease when you add a variable

b. \bar{R}^2 can be negative

c. If the F-test rejects H_0, all coefficients must be significant

d. A high R^2 proves the model is correctly specified

e. The p-value for the F-test can be different from p-values for individual t-tests

Key Terms Introduced: - Coefficient of multiple determination (R^2) - Adjusted coefficient of determination (\bar{R}^2) - ANOVA F-test for overall model - Partial regression coefficient tests - Marginal significance - p-value interpretation

Earlier we identified the danger of multicollinearity—one of the most insidious problems in multiple regression analysis. This issue arises when one or more independent variables are linearly related to each other, violating a fundamental assumption of multiple regression.

WarningDefinition: Multicollinearity

Multicollinearity exists when two or more independent variables are highly correlated with each other.

Simple example:

If X_3 = X_1 + X_2 or X_1 = 0.5X_2, then a linear relationship exists between independent variables.

Why it matters:

Multicollinearity can cause coefficients to have signs opposite to what logic dictates, while vastly inflating the standard errors of the coefficients—making good variables appear insignificant.

13.12.1 Understanding the Problem

Consider a demand model where you’re trying to predict consumer demand for your product. Recognizing that the number of consumers affects demand, you include three explanatory variables:

- X_1 = All males in the market area

- X_2 = All females in the market area

- X_3 = Total population in the market area

The problem: Obviously, X_3 = X_1 + X_2. The total population is an exact linear combination of males and females! The correlations between these variables will be extremely high: - r_{13} (correlation between X_1 and X_3) ≈ very high - r_{23} (correlation between X_2 and X_3) ≈ very high

This guarantees the presence of multicollinearity and creates serious problems for regression analysis.

13.12.2 Multicollinearity in the Hop Scotch Model

Let’s examine whether multicollinearity affects our Hop Scotch Airlines model. From the Python output, we can calculate the correlation matrix:

Correlations: PASS, ADV, NI

ADV PASS

PASS 0.968

NI 0.870 0.903Key observations: - Correlation between PASS and ADV: r = 0.968 (very strong, as expected)

- Correlation between PASS and NI: r = 0.903 (very strong, as expected)

- Correlation between ADV and NI: r = 0.870 ⚠️ (concerningly high!)

The high correlation (0.870) between the two independent variables suggests multicollinearity may be present.

13.12.3 A. Problems Caused by Multicollinearity

ImportantSeven Major Problems Multicollinearity Creates

1. Inability to Separate Individual Effects

When multicollinearity is present, it’s impossible to untangle the individual effects of each X_i on Y. The regression cannot determine how much of the change in Y is due to X_1 versus X_2.

Example: In a model \hat{Y} = 40 + 10X_1 + 80X_2 where X_1 and X_2 are highly correlated, the coefficient of 10 for X_1 may not represent its true effect on Y. The coefficients become unreliable estimates.

2. Inflated Standard Errors

Standard errors of coefficients (S_{b_i}) become excessively large. Taking multiple samples of the same size would show huge variation in the estimated coefficients. One sample might give b_1 = 10, another might give b_1 = 15 or 20.

3. Wrong Signs on Coefficients

Multicollinearity can cause coefficient signs to contradict logic and theory. For example, if price is included in a demand model, you might find it has a positive coefficient—implying consumers buy MORE as price increases! This violates basic economic theory.

4. High Correlations Between Independent Variables

The correlation matrix reveals high values of r_{ij} between independent variables, and the Variance Inflation Factor (VIF) becomes elevated.

5. Coefficient Instability

Large changes in coefficients or their signs occur when the number of observations changes by just one observation. The model becomes extremely sensitive to small data changes.

6. Significant F-ratio with Insignificant t-ratios

The overall F-test shows the model is significant, but individual t-tests show none (or few) of the coefficients are significant. This paradox is a classic symptom of multicollinearity.

7. Large Changes from Adding/Removing Variables

Adding or deleting a single variable produces drastic changes in the remaining coefficients or their signs.

13.12.4 B. Detecting Multicollinearity

There are several methods to detect multicollinearity. Let’s examine each using the Hop Scotch example.

13.12.4.1 Method 1: Correlation Matrix Analysis

The most direct approach is to examine the correlation matrix for all variables in the model.

From Table 13.6, we found r_{12} = 0.870 between advertising (ADV) and national income (NI).

Question: Is 0.870 high enough to indicate problematic multicollinearity?

Unfortunately, there’s no magic cutoff value. Multicollinearity is a matter of degree. Some general guidelines:

- |r_{ij}| < 0.50: Probably not a concern

- 0.50 \leq |r_{ij}| < 0.70: Monitor the situation

- 0.70 \leq |r_{ij}| < 0.85: Likely problematic

- |r_{ij}| \geq 0.85: Almost certainly problematic

For Hop Scotch: r = 0.870 is in the “likely problematic” range, suggesting multicollinearity is present.

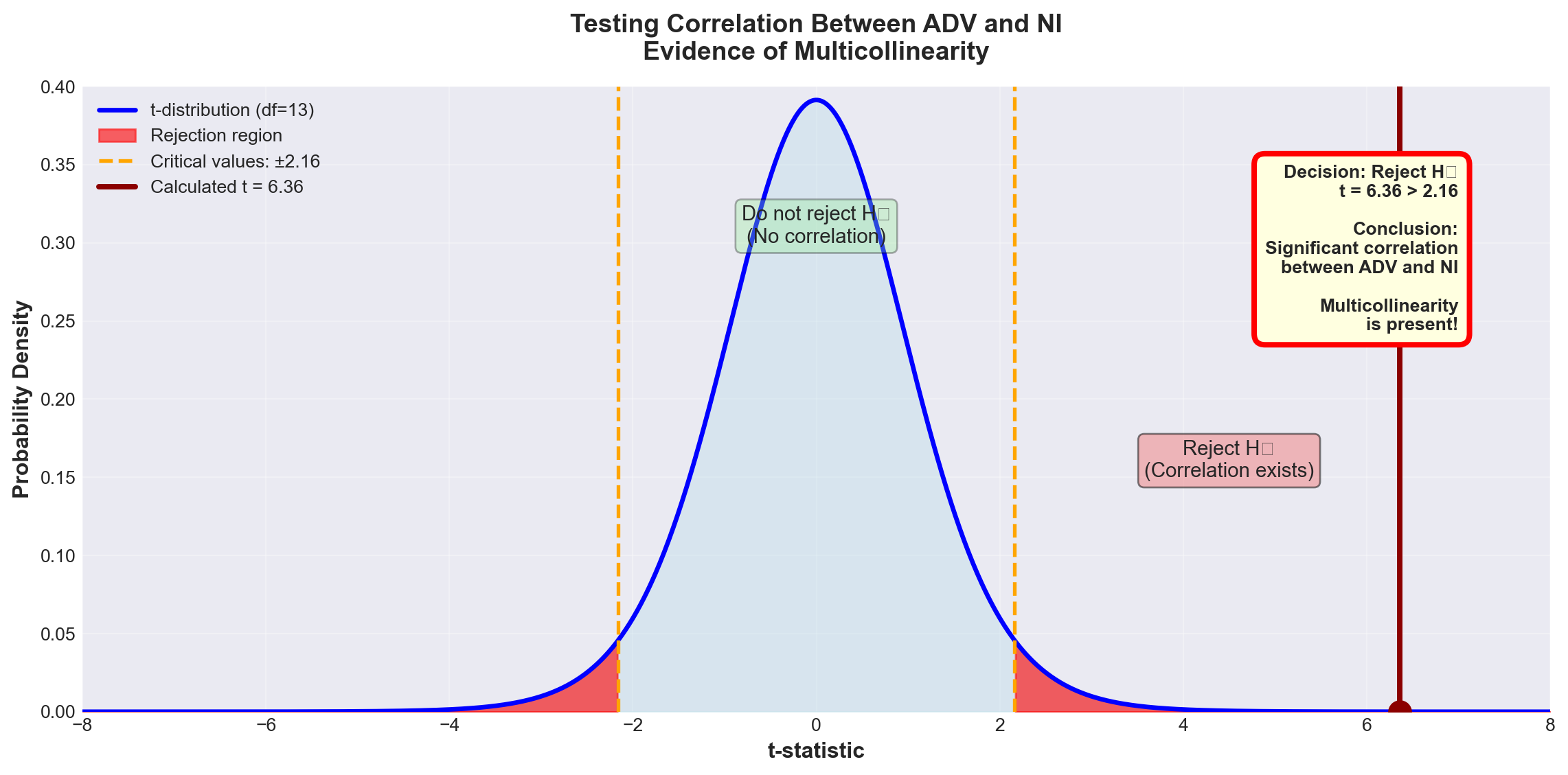

13.12.4.2 Method 2: Hypothesis Test for Correlation

We can formally test whether the population correlation \rho_{12} between the two independent variables differs significantly from zero.

NoteTesting for Significant Correlation Between Independent Variables

Hypotheses: H_0: \rho_{12} = 0 \quad \text{(no correlation)} H_A: \rho_{12} \neq 0 \quad \text{(correlation exists)}

Test statistic: t = \frac{r_{12}}{S_r}

Where: S_r = \sqrt{\frac{1 - r_{12}^2}{n - 2}}

Degrees of freedom: n - 2 (NOT n - k - 1)

Why? We’re testing correlation between just two variables, not testing the full regression model.

For Hop Scotch:

\begin{aligned} S_r &= \sqrt{\frac{1 - (0.870)^2}{15 - 2}} \\ &= \sqrt{\frac{1 - 0.7569}{13}} \\ &= \sqrt{\frac{0.2431}{13}} \\ &= \sqrt{0.0187} \\ &= 0.1367 \end{aligned}

t = \frac{0.870}{0.1367} = 6.36

Test at \alpha = 0.05: - Critical value: t_{0.05, 13} = \pm 2.16 - Decision rule: Reject H_0 if |t| > 2.16

Code

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Create figure

fig, ax = plt.subplots(figsize=(12, 6))

# t-distribution parameters

df = 13

x = np.linspace(-8, 8, 1000)

y = stats.t.pdf(x, df)

# Plot the t-distribution

ax.plot(x, y, 'b-', linewidth=2.5, label=f't-distribution (df={df})')

ax.fill_between(x, 0, y, alpha=0.3, color='lightblue')

# Critical values

t_critical = 2.16

t_calculated = 6.36

# Shade rejection regions

x_left = x[x <= -t_critical]

y_left = stats.t.pdf(x_left, df)

ax.fill_between(x_left, 0, y_left, alpha=0.6, color='red', label='Rejection region')

x_right = x[x >= t_critical]

y_right = stats.t.pdf(x_right, df)

ax.fill_between(x_right, 0, y_right, alpha=0.6, color='red')

# Mark critical values

ax.axvline(-t_critical, color='orange', linestyle='--', linewidth=2,

label=f'Critical values: ±{t_critical}')

ax.axvline(t_critical, color='orange', linestyle='--', linewidth=2)

# Mark calculated t-value

ax.axvline(t_calculated, color='darkred', linestyle='-', linewidth=3,

label=f'Calculated t = {t_calculated}')

ax.plot(t_calculated, stats.t.pdf(t_calculated, df), 'o',

color='darkred', markersize=12)

# Add annotations

ax.text(0, 0.3, 'Do not reject H₀\n(No correlation)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightgreen', alpha=0.3))

ax.text(4.5, 0.15, 'Reject H₀\n(Correlation exists)',

fontsize=11, ha='center',

bbox=dict(boxstyle='round', facecolor='lightcoral', alpha=0.5))

# Labels and formatting

ax.set_xlabel('t-statistic', fontsize=12, fontweight='bold')

ax.set_ylabel('Probability Density', fontsize=12, fontweight='bold')

ax.set_title('Testing Correlation Between ADV and NI\nEvidence of Multicollinearity',

fontsize=14, fontweight='bold', pad=15)

ax.set_xlim(-8, 8)

ax.set_ylim(0, 0.4)

ax.legend(loc='upper left', fontsize=10, framealpha=0.9)

ax.grid(True, alpha=0.3)

# Add decision box

decision_text = (

'Decision: Reject H₀\n'

't = 6.36 > 2.16\n\n'

'Conclusion:\n'

'Significant correlation\n'

'between ADV and NI\n\n'

'Multicollinearity\n'

'is present!'

)

ax.text(7, 0.35, decision_text, fontsize=10, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.6', facecolor='lightyellow',

edgecolor='red', linewidth=3),

verticalalignment='top', horizontalalignment='right')

plt.tight_layout()

plt.show()

ImportantTest Results

Decision: Since t = 6.36 > 2.16, we reject H_0 at the 5% significance level.

Conclusion:

There is statistically significant correlation between advertising and national income (\rho_{12} \neq 0). Some degree of multicollinearity exists in the model.

Important note:

This doesn’t mean the model is fatally flawed. Very few models are completely free of multicollinearity. The question is whether the multicollinearity is severe enough to undermine the model’s usefulness.

13.12.4.3 Method 3: Comparing r^2 Values

Another detection method compares the coefficients of determination between Y and each independent variable individually.

From the correlation matrix: - Passengers and Advertising: r^2 = (0.968)^2 = 0.937 (93.7%) - Passengers and National Income: r^2 = (0.903)^2 = 0.815 (81.5%)

However, when both variables are in the model together: - Multiple regression: R^2 = 0.953 (95.3%)

Analysis:

Taken independently, the two variables explain 93.7% and 81.5% of passenger variation. But together they only explain 95.3%—barely more than advertising alone!

What this means:

There’s substantial overlap in their explanatory power. Much of the information about passengers already provided by advertising is simply duplicated by national income. This overlap is a telltale sign of multicollinearity.

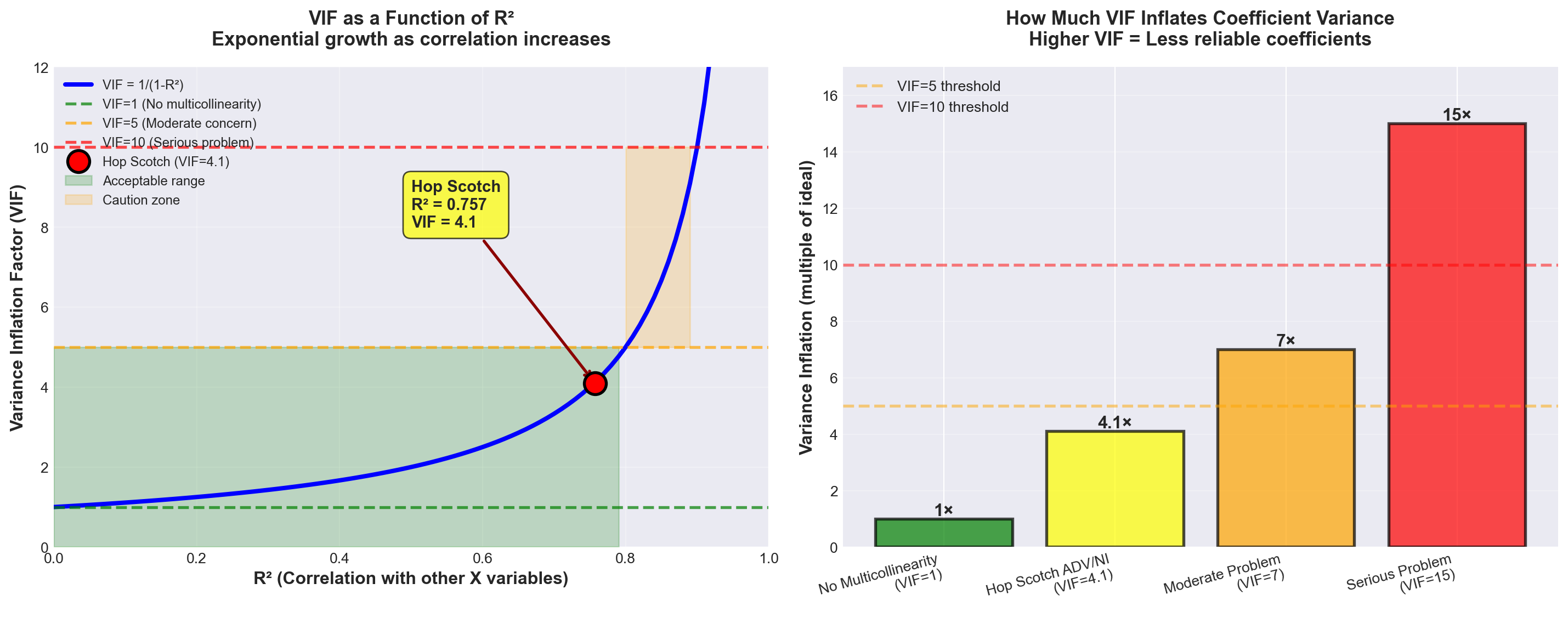

13.12.4.4 Method 4: Variance Inflation Factor (VIF)

The Variance Inflation Factor is a quantitative measure of how much multicollinearity inflates the variance of a regression coefficient.

NoteVariance Inflation Factor (VIF)

For independent variable X_i:

\text{VIF}(X_i) = \frac{1}{1 - R_i^2}

Where:

R_i^2 = Coefficient of determination from regressing X_i on all other independent variables

Interpretation:

The VIF measures how much the variance of b_i is inflated above what it would be if there were no multicollinearity.

Rules of thumb: - VIF = 1: No correlation with other variables (ideal) - VIF < 5: Low multicollinearity (acceptable) - 5 ≤ VIF < 10: Moderate multicollinearity (concerning) - VIF ≥ 10: High multicollinearity (serious problem) - Sum of all VIFs ≥ 10: Overall model multicollinearity concern

For Hop Scotch:

Since we have only two independent variables, regressing each on the other gives the same r = 0.870.

Therefore: R^2 = (0.870)^2 = 0.7569

\text{VIF}(\text{ADV}) = \text{VIF}(\text{NI}) = \frac{1}{1 - 0.7569} = \frac{1}{0.2431} = 4.1

From Python output (Screen 12.6):

Both VIF values show 4.1 ✓

Code

import numpy as np

import matplotlib.pyplot as plt

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

# Create figure with two subplots

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 6))

# Left plot: VIF vs R²

r_squared = np.linspace(0, 0.99, 100)

vif = 1 / (1 - r_squared)

ax1.plot(r_squared, vif, 'b-', linewidth=3, label='VIF = 1/(1-R²)')

ax1.axhline(y=1, color='green', linestyle='--', linewidth=2, alpha=0.7, label='VIF=1 (No multicollinearity)')

ax1.axhline(y=5, color='orange', linestyle='--', linewidth=2, alpha=0.7, label='VIF=5 (Moderate concern)')

ax1.axhline(y=10, color='red', linestyle='--', linewidth=2, alpha=0.7, label='VIF=10 (Serious problem)')

# Mark Hop Scotch point

hop_scotch_r2 = 0.7569

hop_scotch_vif = 4.1

ax1.plot(hop_scotch_r2, hop_scotch_vif, 'ro', markersize=15,

markeredgecolor='black', markeredgewidth=2, label='Hop Scotch (VIF=4.1)', zorder=5)

ax1.annotate('Hop Scotch\nR² = 0.757\nVIF = 4.1',

xy=(hop_scotch_r2, hop_scotch_vif), xytext=(0.5, 8),

fontsize=11, fontweight='bold',

bbox=dict(boxstyle='round,pad=0.5', facecolor='yellow', alpha=0.7),

arrowprops=dict(arrowstyle='->', lw=2, color='darkred'))

# Add shaded regions

ax1.fill_between(r_squared[vif <= 5], 0, 5, alpha=0.2, color='green', label='Acceptable range')

ax1.fill_between(r_squared[(vif > 5) & (vif <= 10)], 5, 10, alpha=0.2, color='orange', label='Caution zone')

ax1.set_xlabel('R² (Correlation with other X variables)', fontsize=12, fontweight='bold')

ax1.set_ylabel('Variance Inflation Factor (VIF)', fontsize=12, fontweight='bold')

ax1.set_title('VIF as a Function of R²\nExponential growth as correlation increases',

fontsize=13, fontweight='bold', pad=15)

ax1.set_ylim(0, 12)

ax1.set_xlim(0, 1)

ax1.legend(loc='upper left', fontsize=9)

ax1.grid(True, alpha=0.3)

# Right plot: Variance inflation visualization

categories = ['No Multicollinearity\n(VIF=1)', 'Hop Scotch ADV/NI\n(VIF=4.1)',

'Moderate Problem\n(VIF=7)', 'Serious Problem\n(VIF=15)']

vif_values = [1, 4.1, 7, 15]

colors = ['green', 'yellow', 'orange', 'red']

bars = ax2.bar(categories, vif_values, color=colors, edgecolor='black', linewidth=2, alpha=0.7)

# Add value labels on bars

for bar, val in zip(bars, vif_values):

height = bar.get_height()

ax2.text(bar.get_x() + bar.get_width()/2., height,

f'{val}×',

ha='center', va='bottom', fontsize=12, fontweight='bold')

# Add reference lines

ax2.axhline(y=5, color='orange', linestyle='--', linewidth=2, alpha=0.5, label='VIF=5 threshold')

ax2.axhline(y=10, color='red', linestyle='--', linewidth=2, alpha=0.5, label='VIF=10 threshold')

ax2.set_ylabel('Variance Inflation (multiple of ideal)', fontsize=12, fontweight='bold')

ax2.set_title('How Much VIF Inflates Coefficient Variance\nHigher VIF = Less reliable coefficients',

fontsize=13, fontweight='bold', pad=15)

ax2.set_ylim(0, 17)

ax2.legend(loc='upper left', fontsize=10)

ax2.grid(True, alpha=0.3, axis='y')

# Rotate x-axis labels

ax2.set_xticks(range(len(categories)))

ax2.set_xticklabels(categories, rotation=15, ha='right')

plt.tight_layout()

plt.show()

TipInterpreting VIF = 4.1 for Hop Scotch

What it means:

The variance of the coefficient estimates for advertising and national income is 4.1 times larger than it would be if there were no multicollinearity.

Is this a problem?

VIF = 4.1 is in the low to moderate range: - Below the VIF = 5 “concern” threshold - Well below the VIF = 10 “serious problem” threshold - Sum of VIFs = 4.1 + 4.1 = 8.2 (below the 10 threshold)

Verdict:

While multicollinearity is present, it’s not severe enough to completely undermine the model. We should be aware of it and monitor for its effects, but it’s not a fatal flaw.

13.12.5 Other Indicators of Multicollinearity

Beyond the formal detection methods, watch for these warning signs:

5. Large coefficient changes from small sample changes

If adding or removing just one observation causes dramatic shifts in coefficient values or signs, multicollinearity is likely present.

6. Significant F-ratio with insignificant t-ratios

In our Hop Scotch model: - Overall F-test: F = 121.18 (highly significant, p < 0.001) - Advertising t-test: t = 5.92 (significant, p < 0.001) - National Income t-test: t = 1.96 (not significant at α = 0.05, p = 0.074)